When businesses evaluate a recurring payment solution, most of the attention is placed on mandate registration. Questions like “How quickly can customers authorize?” or “Which mandate method should we use NACH or UPI AutoPay?” often dominate discussions.

However, mandate registration is only the beginning.

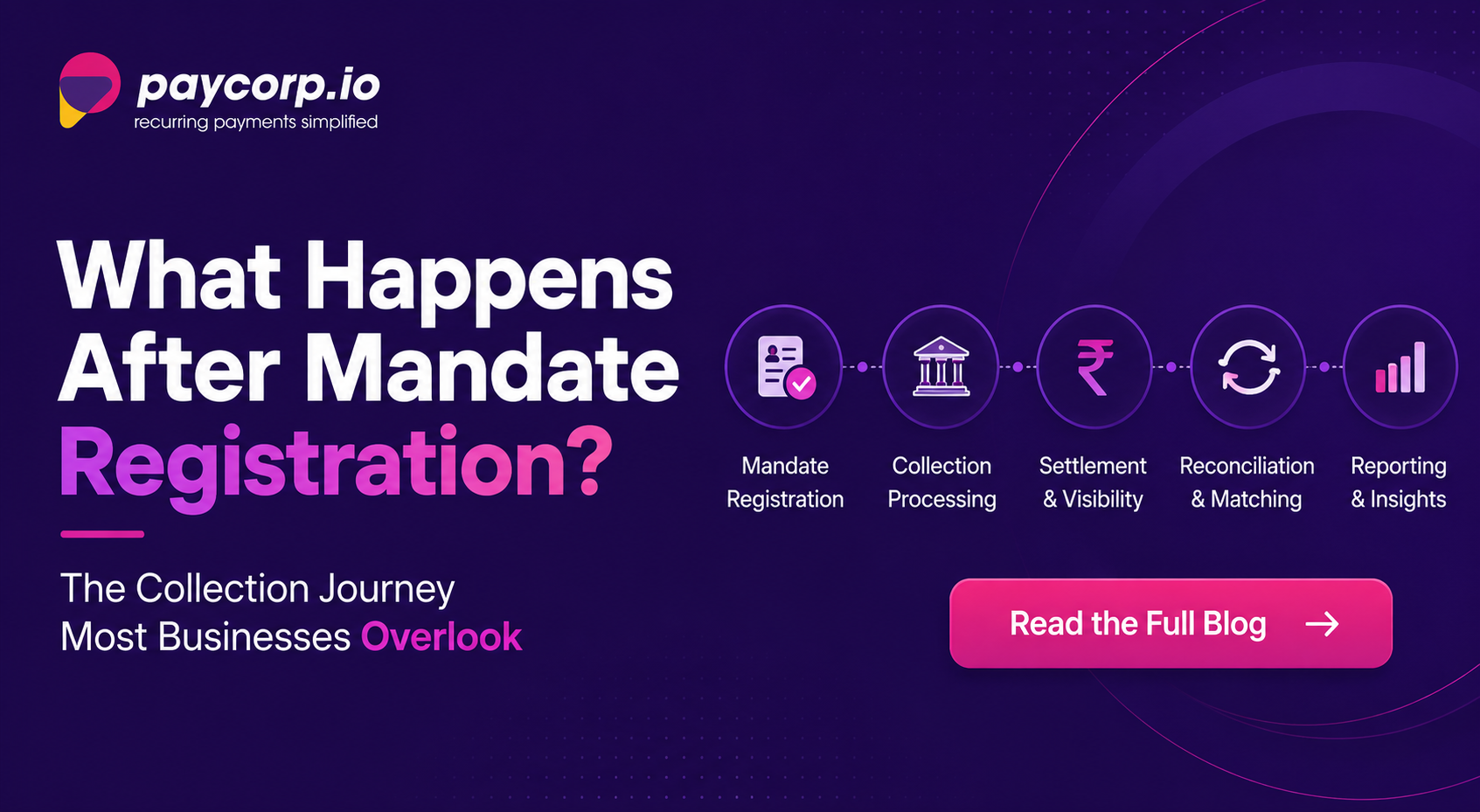

The real challenge starts after the mandate is approved. This is where collections, settlement cycles, reconciliation, reporting, and exception handling determine whether your recurring payment infrastructure drives efficiency or creates operational bottlenecks.

For NBFCs, fintechs, lenders, insurance companies, and subscription businesses, understanding the complete collection journey is critical to maximizing recovery rates and improving customer experience.

Step 1: Mandate Registration

The journey begins with eMandate Registration, where customers authorize recurring debits from their bank account.

Businesses today typically leverage:

- NACH Software for recurring collections through bank accounts

- UPI AutoPay Mandates for digital-first customer onboarding

- Hybrid recurring payment models combining both methods

At this stage, customer onboarding is completed and the mandate is approved.

Many businesses mistakenly believe the difficult part is over.

In reality, the collection journey has just begun.

Step 2: Collection Presentation

Once the mandate becomes active, debit requests are initiated according to the agreed collection schedule.

This is where collection efficiency becomes critical.

Common challenges include:

- Insufficient account balance

- Incorrect debit dates

- Customer account changes

- Bank-level rejections

- Collection processing delays

A robust Recurring Payment API enables businesses to automate debit scheduling, monitor collection status, and manage exceptions without manual intervention.

The ability to track collections in real time can significantly reduce operational overhead and improve visibility.

Step 3: Managing Collection Failures

Collection failures are one of the biggest sources of revenue leakage for lenders and recurring payment businesses.

Traditional collection processes often rely on manual follow-ups and delayed recovery attempts.

Modern Recurring Payment Solutions address this through:

- Automated retry mechanisms

- Real-time status updates

- Intelligent collection routing

- Faster failure identification

For organizations processing thousands of mandates every month, even a small improvement in success rates can result in significant revenue impact.

Step 4: Settlement and Fund Visibility

Successfully collecting payments is only one part of the equation.

Businesses also need:

- Faster settlements

- Accurate fund tracking

- Visibility into payment flows

- Improved cash flow management

Delayed settlements can impact liquidity and operational planning, especially for lenders and NBFCs managing large collection volumes.

This is why modern collection infrastructure focuses not only on collection success but also on faster settlement processing and reporting.

Step 5: Reconciliation : The Most Overlooked Process

For many businesses, reconciliation remains one of the most time-consuming operational activities.

Teams often spend hours matching:

- Mandates

- Collections

- Settlements

- Failed transactions

- Customer records

Without proper automation, reconciliation can become a major operational burden.

A scalable Recurring Payment Solution should provide:

- Real-time reporting

- Automated reconciliation

- Collection-level visibility

- Exception management

This helps finance and operations teams focus on growth instead of manual tracking.

When Traditional Collection Models Fall Short

As lending and financial services evolve, collection requirements are becoming increasingly complex.

Consider these scenarios:

Co-Borrower Loans

A loan may involve multiple contributors who share repayment responsibility.

Joint Account Holders

Customers may prefer splitting payments across multiple accounts.

Shared Financial Commitments

Insurance, lending, and subscription models increasingly involve more than one contributor.

Traditional mandate structures were designed for a single payer.

Modern businesses need greater flexibility.

The Rise of Split Mandates

To address these challenges, many organizations are exploring more advanced collection models.

One such innovation is the Split Mandate approach.

Instead of collecting the entire amount from a single account, businesses can define how collections are distributed among multiple contributors while maintaining a unified collection structure.

For example:

- Borrower A contributes 40%

- Borrower B contributes 30%

- Borrower C contributes 30%

The total collection obligation remains unchanged, while repayment responsibility is distributed across contributors.

This creates flexibility for:

- Co-lending models

- Joint borrowers

- Shared EMI structures

- Multi-contributor payment ecosystems

How Paycorp Helps Businesses Build Smarter Collection Infrastructure

At Paycorp, we believe recurring collections should extend beyond mandate registration.

Our platform enables businesses to manage the complete recurring payment lifecycle through:

NACH Automation

End-to-end mandate registration, collection processing, settlement visibility, and reporting.

UPI AutoPay

Digital-first recurring payment experiences with faster customer onboarding.

Recurring Payment APIs

Seamless integration capabilities for lenders, NBFCs, fintechs, and enterprise businesses.

Smart Collection Management

Automated retries, collection tracking, and reconciliation support.

Split Mandate Capability

Support for advanced collection models involving multiple contributors while maintaining complete visibility and operational control.

Real-World Example

Imagine an NBFC offering education loans with a parent and student as co-borrowers.

Traditionally, collections would depend on a single account.

If that account faces insufficient funds, the EMI may fail.

With a more flexible collection framework, repayment obligations can be distributed across multiple contributors, reducing collection risk and improving payment success rates.

The result:

- Better customer experience

- Improved collection efficiency

- Reduced operational complexity

- Greater payment flexibility

Conclusion

Mandate registration is only the first step in the recurring payment journey.

The real value lies in what happens afterward collection management, failure handling, settlements, reconciliation, and customer flexibility.

As recurring payment ecosystems continue to evolve, businesses need infrastructure that goes beyond basic mandate processing.

Whether you’re leveraging NACH Software, UPI AutoPay for Recurring Payments, eMandates, or advanced capabilities like Split Mandates, success depends on building a collection framework that is automated, scalable, and designed for the realities of modern financial services.

The organizations that optimize the entire collection journey not just mandate registration will be the ones that achieve higher collection efficiency, better customer experiences, and sustainable growth.